Iowa Short Term Health Insurance

A Short Term Medical Plan is temporary medical insurance that provides comprehensive protection against unexpected health care health care expenses. Policies can be purchased from 30 to 90 days. The application process is simple with only a few qualifying questions to answer and coverage can begin as early as the next day.

Short Term Medical Insurance is perfect for individuals who are:

- Recent college graduates

- Between jobs or laid off

- Waiting for employer-sponsored coverage

- Losing dependent status

- Looking for a lower-cost alternative to COBRA

- Recently retired and not eligible for Medicare

- On strike

UHC Short Term Insurance

![]()

More About UHC

Company Information

Short term limited duration health insurance is designed to provide a fast, flexible, and budget-friendly option to help bridge a gap in coverage.

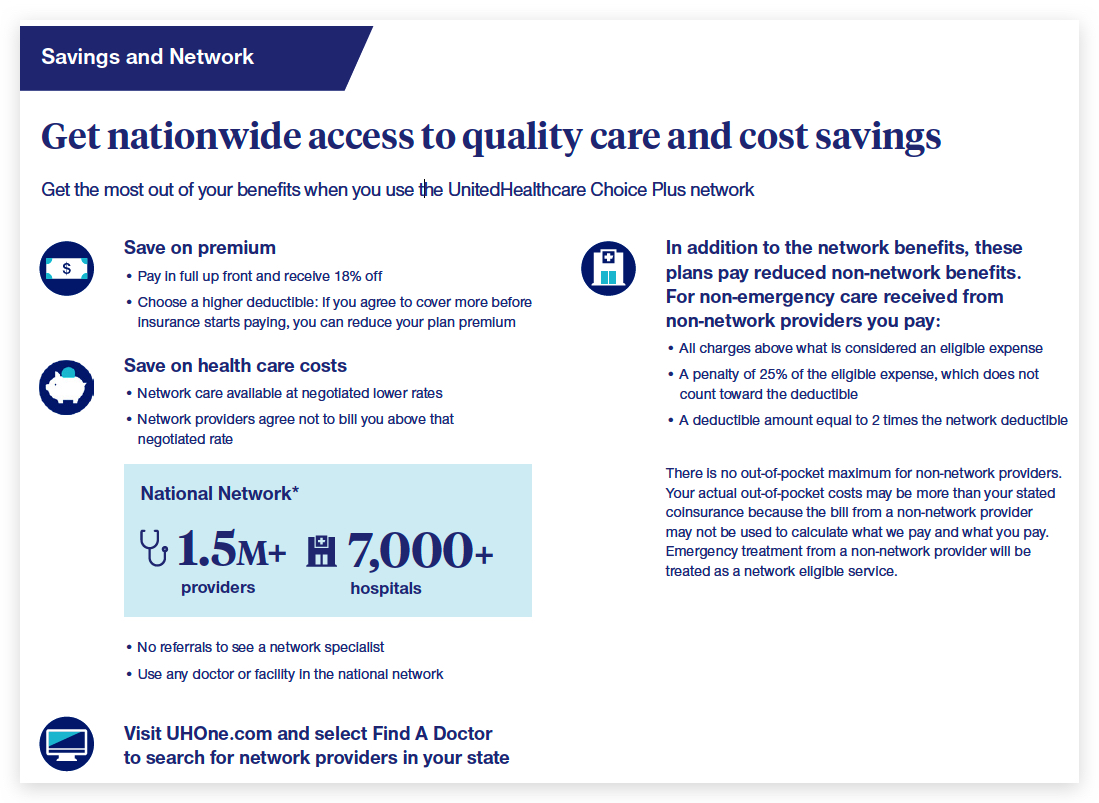

UnitedHealthcare Choice Network (EPO) DE, FL, IA, IN, KS, LA, MI, MO, MS, NE, NV, PA, SC, TN, TX, WI, WV, WY: There are no non-network benefits. You must use a network doctor or hospital. These plans pay no benefits for out-of-network expenses except for emergencies. Emergency treatment from a non-network provider will be treated as network eligible service.

Short-Term Medical Secure Plans – Plan Comparison

| Plan Designs | Secure Edge | Secure Bridge | Secure Net |

|---|---|---|---|

| Office visit copay | $50 – 1 copay for 30-90 days 2 copays for 91-180 days 3 copays for 181-364 days | $50 – 1 copay for 30-90 days/ 2 copays for 91-180 days 3 copays for 181-364 days | $50 – 1 copay for 30-90 days/ 2 copays for 91-180 days/ 3 copays for 181-364 days |

| Deductible | $1,000 $2,500 $5,000 $7,500 | $1,000 $1,500 $2,500 $5,000 $7,500 $10,000 | In-Network: $3,500 $5,000 $7,500 $10,000 Out-of-network deductible is two times the in-network deductible. |

| Coinsurance and out-of-pocket (not including deductible) | 20% – $1,000, $2,000, $3,000, $4,000 50% – $2,500, $5,000, $7,500, $10,000 | 20% – $1,000, $2,000, $3,000, $4,000 30% – $1,500, $3,000, $4,500, $6,000 50% – $2,500, $5,000, $7,500, $10,000 | In-Network: 0%1 – $0 20% – $3,500, $5,000, $7,500, $10,000 30% – $3,500, $5,000, $7,500, $10,000 Out-of-network coinsurance is 50% and the out-of-pocket is two times the in- network out-of-pocket ($7,000 for 0%/$0). |

| Maximum benefit | $1,000,000 | $2,000,000 | $2,000,000 |

| Covered Expenses | Secure Edge | Secure Bridge | Secure Net |

|---|---|---|---|

| Doctor administering anesthetics | Up to 20% of the surgeon’s benefit2 | Up to 20% of the surgeon’s benefit | No benefit-specific limit |

| Assistant surgeon | Up to 20% of the surgeon’s benefit2 | Up to 20% of the surgeon’s benefit | No benefit-specific limit |

| Surgeon’s assistant | Up to 15% of the surgeon’s benefit2 | Up to 15% of the surgeon’s benefit | No benefit-specific limit |

| Ambulance, ground or air services | Up to $250 per occurrence | Ground: Up to $500 per occurrence Air: Up to $1,000 per occurrence | No benefit-specific limit |

| Organ, tissue or bone marrow transplants | Up to $150,000 per coverage period | Up to $150,000 per coverage period | Up to $150,000 per coverage period |

| Acquired Immune Deficiency Syndrome (AIDS) | Up to $10,000 per coverage period | Up to $10,000 per coverage period | Up to $10,000 per coverage period |

| Emergency room | Up to $500 per day | No benefit-specific limit | No benefit-specific limit |

| Outpatient hospital surgery or ambulatory surgical center | Up to $1,000 per day | No benefit-specific limit | No benefit-specific limit |

| Hospital room, board and general nursing care | The amount billed for semi- private room or 90% of the private room billed amount, up to $5,000 per day | The amount billed for semi- private room or 90% of the private room billed amount | The amount billed for semi-private room or 90% of the private room billed amount |

| Intensive care unit | Three times the amount billed for a semi-private room or three times 90% of the private room billed amount, up to $6,250 per day | Three times the amount billed for a semi-private room or three times 90% of the private room billed amount | Three times the amount billed for a semi- private room or three times 90% of the private room billed amount |

| Inpatient doctor visits | Up to $500 per confinement | No benefit-specific limit | No benefit-specific limit |

All plans Include one-time $25 enrollment fee

UHC Provider Network

Through the STM plan, you have access to the UnitedHealthcare Choice Network (EPO) DE, FL, IA, IN, KS, LA, MI, MO, MS, NE, NV, PA, SC, TN, TX, WI, WV, WY: There are no non-network benefits. You must use a network doctor or hospital. These plans pay no benefits for out-of-network expenses except for emergencies. Emergency treatment from a non-network provider will be treated as network eligible service.

National General Short Term Medical

More About National General

Company Information

National General’s Short Term Medical insurance gives you a plan to face those unpredictable moments in life with confidence. It provides the financial protection you need from unexpected medical bills and other health care expenses, including:

- Doctor visits and some preventive care

- Emergency room and ambulance coverage

- Urgent care benefits, and more

National General Health Insurance Feature Highlights

- Coverage Period Maximum of $250,000 and $1,000,000

- Deductible options of $1,000, $2,500, or $5,000

- Coinsurance Percentage of In-Network plan 100/0, 80/20 and 50/50

- Doctor Office Visit and Urgent Care Co-pay of $50

Standard Issue Plans

| Deductible* | Coinsurance | Out-Of-Pocket Max | Coverage Period Max |

|---|---|---|---|

| $1,000 | 50% / 50% | $2,500 | $250,000 |

| 80% / 20% | $1,500 | $1,000,000 | |

| $2,500 | 50% / 50% | $2,500 | $250,000 |

| 80% / 20% | $1,500 | $1,000,000 | |

| 100% | $0 | $1,000,000 | |

| $5,000 | 50% / 50% | $3,750 | $250,000 |

| 80% / 20% | $2,000 | $1,000,000 | |

| 100% | $0 | $1,000,000 | |

| $10,000 | 100% | $0 | $1,000,000 |

| $25,000 | 100% | $0 | $1,000,000 |

* Per-person deductible and out-of-pocket amounts are capped at 3x the individual amounts for a family greater than three. This means that when three insured family members satisfy their individual deductibles and out-of-pocket amounts, the remaining individual deductibles and out-of-pocket amounts will be deemed as satisfied for the remainder of the coverage term. 2 Short Term Medical plans do not cover costs associated with pre-existing conditions.

National General Provider Network

Choose Your Provider

National General’s Short Term Medical insurance gives you access to the Aetna Open Choice PPO network, one of the largest networks in the country with no referral required.

Short Term Health Insurance and Network Breadth

While more than half of ACA plans lack out-of-network coverage,14 all short term insurance plans offered through AgileHealthInsurance have broad network coverage ensuring that an enrollee has access to quality health care providers. If an enrollee goes out of network and finds that the provider does not accept their short term insurance, in many cases, the enrollee can get reimbursed by submitting their claim to the insurance company. To be sure, enrollees should check with their insurance company first.

Short Term insurance plan premiums are also significantly less expensive than unsubsidized premiums for health plans sold on the exchanges. Compared to the average costs for 2016 Obamacare bronze plans for individuals aged 30, 40, and 50, short term insurance plans are 25 percent less expensive. Savings are greater for younger individuals without pre-existing conditions. For healthy males, aged 30, a short term insurance premium is 54.93% less expensive than an Obamacare Bronze plan.15

It should be noted that unlike ACA plans, short term insurance plans do not cover medical conditions that existed prior to enrollment.

Short Term Health Insurance FAQ

How Is Short Term Health Insurance Different Than Obamacare?

Affordable Care Act plans typically have broader benefits than found in Short Term health insurance and, without the premium subsidies available to some qualified purchasers, cost much more than Short Term plans.

All health plans that fit in the Affordable Care Act must have “10 Essential Health Benefits.” Short Term health insurance plans, in comparison, do not have a standardized set of benefits. Short Term plans usually offer what would be described as “major medical coverage” that covers healthcare costs in the event of serious medical issues. Most Short Term plans also cover normal doctor visits for routine illnesses and injuries.

Considering the prevalence of ACA insurance plans with narrow networks, consumers should heavily research plans before enrolling to ensure that they are not putting themselves at risk for high out-of-network costs.

For those needing broad coverage, short term insurance may be a good option. 100 percent of short term insurance plans sold through Independent Health Agents have out-of-network coverage. Enrollees in these plans can be ensured that they will have access to high quality providers without incurring unknown and potentially sizable costs.

The chart below details some of the major benefit differences between Short Term health insurance plans and Affordable Care Act plans. It is important to note that Affordable Care Act plans do not deny care for pre-existing conditions nor do they reject applicants based on health problems.

| Short Term Health Insurance Plans | Affordable Care Act Plans | |

| Coverage availability | Apply any time and get coverage as early as the next day | Apply only during Open Enrollment (or Special Enrollment due to a qualifying event) and get coverage in 2-6 weeks |

| Coverage duration | Coverage duration is less than three months. Many plans can be cancelled at any time. | As long as the plan is available. You can change plans during Open Enrollment (or Special Enrollment with a qualifying event) |

| Prescription drug coverage | Many Short Term health insurance plans provide a drug discount card but do not provide drug coverage. Some newer plans have a prescription drug coverage option for generic drugs not associated with a pre-existing condition. Brand name drugs and specialty drugs are typically uncovered. | Minimum of 1 drug per class must be covered but the minimum number of drugs per class is often more due to the benchmark chosen for each particular state. |

| Maternity and newborn care | Complications of maternity are covered but not standard childbirth services. | Full coverage. Applicants cannot be denied based on pregnancy as a precondition. |

| Mental health services | Coverage is included only when mandated at state level. | Coverage included, but states vary on their definition of “mental health” services, so while some do include learning disabilities or conditions like Autism, other states do not. |

| Substance use disorder services | Coverage is included only when mandated at state level. | All ACA plans have full coverage. |

| Rehabilitative and habilitative services | Coverage is included only when mandated at state level. | All ACA plans have full coverage. |

| Preventive care | Some plans have selected preventive care benefits with cost-sharing. However, most plans do not cover preventive care services. | Preventative services must be provided without cost-sharing (cf.https://www.healthcare.gov/preventive-care-benefits) |

| Pediatric services – oral and dental care | Coverage is included only when mandated at state level. | All ACA plans have full coverage. |

| Healthcare provider networks | Short Term plans typically have broad acceptance among healthcare providers. Some have a preferred network with negotiated pricing for healthcare services and a larger non-preferred network where the plans pay ‘usual and customary’ fees for covered healthcare. | These plans have been noted for a significant use of “narrow networks” to increase the ratio of enrollees to healthcare providers. |

| Uninsured tax penalties | The maximum penalty is the national average premium for a bronze plan. For 2016, the tax is 2.5% of modified adjusted gross household income or $695 per person, whichever is greater. | ACA plans meet the requirements for avoiding the tax penalty. |

| Coverage of pre-existing conditions | These plans evaluate health status and pre-existing conditions when processing an insurance application and determine whether the applicant is approved or rejected for coverage. | These plans do not consider health status or pre-existing conditions when processing an insurance application. |

What does short-term health insurance cover?

Is short-term health insurance Obamacare?

No. Short-term health insurance is a streamlined insurance plan. While it includes many benefits, it does not cover all 12 of the minimum essential benefits that the Affordable Care Act plans are required to cover. For example, in most cases, short-term health insurance will not include maternity care or mental health services.

In addition, short-term health insurance involves an application. Depending on your health status, your application may be declined or your pre-existing condition may be excluded. Obamacare guarantees that all applicants and their pre-existing conditions will be covered, no matter what your health status.

When can I apply for short-term health insurance?

Can I cancel a short term plan at any time?

What conditions on the application will make me ineligible for a short term plan?

Within the last 5 years if you have been diagnosed, treated, or taken medication for any of the following conditions, term health insurance cannot be issued: Cancer or tumor, stroke, heart disease including heart attack, chest pain or had heart surgery, COPD (chronic obstructive pulmonary disease) or emphysema, Crohn’s disease, liver disorder, degenerative disc disease, rheumatoid arthritis, kidney disorder, diabetes, degenerative joint disease of the knee, alcohol abuse or chemical dependency, or any neurological disorder; HIV or AIDS; or if you are now pregnant or in the process of adoption.

If you are looking for insurance to cover your pre-existing conditions, we can refer you to an agent who can help you find a health insurance plan that to cover these conditions:

- For ACA/Obamacare Plans: 312-726-6565

Find What Plans Your Doctor Accepts

Find Every Plan In Your Area

Calculate Your Subsidy

Live Chat Our Agents

Apply On Or Off the Exchange

Apply in Under 5 Minutes

What To Know:

- Plans for as little as 30 days up to 180 days. Can cancel anytime.

- Single plan max is 90 days, but you can renew once

- Doesn’t cover pre-existing conditions

- Additional add-on options for accident protection, prescriptions and more